Startups

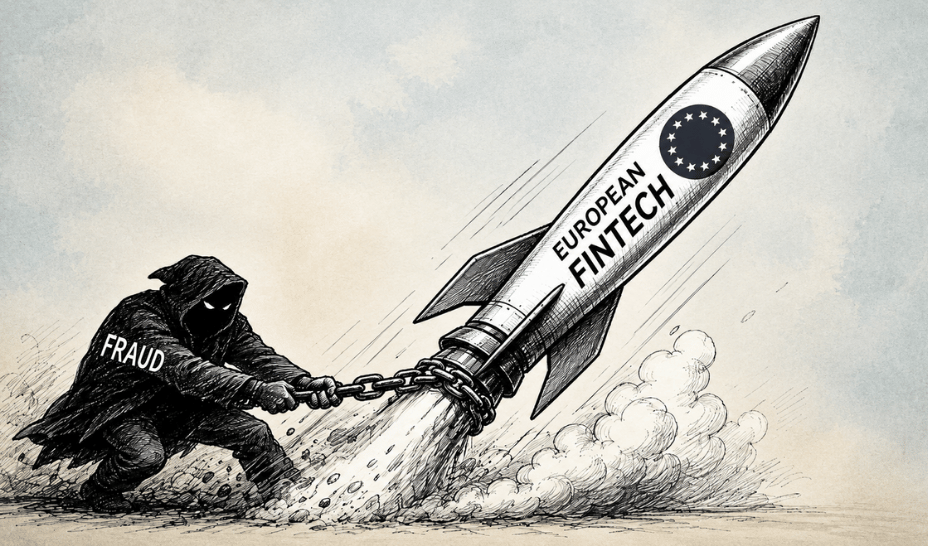

Uncovering the Underbelly of Europe’s FinTech Revolution: The Fraud Threat Lurking in the Shadows

European FinTech has won by making money feel faster, simpler and more intuitive. From instant onboarding to seamless payouts, companies such as Revolut have helped set the standard for what users now expect from financial products.

But every FinTech founder, operator and investor faces the same tension: the smoother the product experience becomes, the more attractive it can be to fraudsters.

Behind the growth of European FinTech, a parallel market has been scaling just as quickly: fraud.

Fraudsters are entrepreneurs as well. They research markets and competitors, identify weak points and build creative ways to exploit complexity. They also puncture the credibility of FinTech – if they continue unchecked, the industry will have to hand over all its gains back to traditional banks.

If you’ve worked in FinTech long enough, you see the trend. A new flow comes into effect. It simplifies the lives of constructive users. After a few weeks, you begin observing the initial case of abuse. Then another one, which is a little different. Then ten more. It arrives as a quiet stream of support tickets and risk alerts, until your product suddenly feels more exposed than expected.

Fraud now runs on software economics

INTERPOL put a number on what many teams are already feeling. In its March 2026 Global Financial Fraud Threat Assessment, it warns that AI-enhanced fraud is estimated to be 4.5 times more profitable than traditional methods, and it points to agentic AI systems that can plan and run full campaigns from reconnaissance to laundering.

That is a different threat model than simply having a few bad actors.

Attackers can now automate targeting, scripting, social engineering, and the cash-out pipeline. All of this is now done with less effort. A defence model that depends mostly on manual review will always be late, because the attacker’s throughput is not tied to headcount and attackers adapt faster than static systems.

This is where the industry has to be honest with itself. If your adversary has automated most of their tasks, you cannot defeat them with numbers of people. But you also cannot blindly automate trust. Automated systems still struggle with context, manipulation tactics, and edge cases, which is exactly where serious fraudsters put their effort.

I consider something more hybrid to be the answer.

The answer is not to replace people with automation. The answer is to use automation for volume and detection, while keeping humans focused on intent, patterns and exceptions. In other words, the answer is a hybrid system.

Digital onboarding is no longer a strong gate

Onboarding is step one in fraud.

Entrust’s 2025 Identity Fraud Report highlights a 244% year-over-year increase in digital document forgeries, and reports that deepfake attempts occurred every five minutes in 2024.

This is what that means on the ground. A fake document is no longer something that looks obviously tampered with. It can be clean, high-resolution, and tailored to pass basic checks. You can also expect more attackers to mix document fraud with social engineering, so even a valid identity can be paired with coerced behaviour later.

Modern defence cannot stop at document verification. Passing KYC doesn’t mean much on its own anymore: the real signal comes afterwards, from behaviour and ongoing due diligence (ODD) and enhanced due diligence (EDD) are extremely important.

Things like device and session signals. Velocity checks. Risk-based step-ups when something looks off. You also need people who know what to look for when verification tools signal a pass but the story does not feel right.

Customers are worried about identity theft

Speed is central to FinTech, but in a sensitive industry, it can also create room for oversight.

Consumer anxiety calls for more caution. Experian’s 2025 U.S. Identity & Fraud Report found identity theft is the top consumer concern at 68%. Users still want to have the speed of FinTech though but accompanied with the confidence that they will be safe if things go awry. They do not want to simply trade their hard-earned money for a convenient model that stops taking responsibility when they are targeted.

That pushes FinTeech toward a smart friction model. That would consist of less blanket review with more targeted intervention. It also means better signals, and a faster response when a scam pattern starts showing up.

Liability is shifting onto payment providers

From traditionally being seen as a matter of security, fraud is now being analysed through the lens of unit economics.

The UK has followed the trajectory of these winds. The Payment Systems Regulator’s authorised push payment scam reimbursement regime went live on 7 October 2024, with a maximum reimbursement level set at £85,000 per claim for Faster Payments.

Europe is moving in a similar direction. In November 2025, the Council and European Parliament announced a provisional political agreement on a new payment services regulation and PSD3 changes, explicitly framed around stepping up the fight against payment fraud.

Once reimbursement and fraud obligations tighten, weak controls shift from being a risk to becoming a predictable margin hit. You pay directly in losses, chargebacks and support load. Then you pay again when excessive friction makes it harder to convert users.

Better fraud prevention is undoubtedly expensive, but so is letting fraud become normal.

The outdated collaboration gap

While fraud groups share playbooks across borders, FinTechs often do not, partly because of privacy law, liability, and reputational risk.

Still, there is a middle ground that the industry underuses.

You do not need to share raw customer data to help each other. You can share typologies, scam structures, and signals. You can share what it looks like rather than who it was. That is often enough to help other teams recognise a pattern earlier.

There are already efforts in this direction.

The European Payments Council has outlined the importance of collaboration in combating fraud across the SEPA region. They emphasize the need for data collection, analysis, and information sharing to stay ahead of attackers. Additionally, there are EU proposals in place that focus on data sharing for fraud prevention efforts.

When it comes to fraud prevention, keeping intelligence as a trade secret can be detrimental. It leads to individuals bearing the learning cost alone, while attackers continue to exploit vulnerabilities across different markets.

For founders and operators looking to enhance their fraud prevention measures, there are several key actions to take. Firstly, implementing controls that are regularly updated is crucial to staying proactive. Onboarding processes should be taken seriously as the first line of defense, followed by diligent post-onboarding monitoring based on user behavior.

It’s essential to design interventions that enhance security without complicating the user experience. Utilizing risk-based step-ups instead of rigid security measures can strike a balance between protection and usability. Viewing fraud prevention as a business cost, rather than just a security expense, is vital for safeguarding revenue and maintaining a seamless product experience.

Over the past decade, FinTech has prioritized user experience and simplicity. Moving forward, the focus should shift towards safeguarding these advancements without introducing unnecessary friction. By implementing these strategies, businesses can protect their progress while maintaining a user-friendly approach.

In conclusion, collaboration, continuous adaptation, and a strategic approach to fraud prevention are essential in the ever-evolving landscape of financial technology. By staying proactive and prioritizing user security, businesses can uphold their commitment to innovation and customer satisfaction while safeguarding against fraudulent activities.

Star Trek: Voyager – Destination Equinox

Databricks soars to $188B valuation, solidifying its position as AI’s ultimate comeback story

Uncovering the True Motives: The Apple vs. OpenAI Legal Battle

Apple Music and Apple One: Pricing Updates and Changes

Revolutionizing Life with Enhanced 3D Printing Technology

Exclusive Interview: GWM Australia COO John Kett Reveals Insider Insights

Fallout 5: A New Chapter Unveiled Amidst Xbox’s Mass Layoffs

Case of Mistaken Identity: Russian Tourist Detained in Armenia for Alleged REvil Hacker Activity

I would defend diversity with all my might: The Sims artist’s battle against mandated homogeneity post-EA Saudi acquisition

EU Takes Action Against Instagram and Facebook for Violating Illegal Content Rules

Warning: Facebook Creators Face Monetization Loss for Stealing and Reposting Videos

Facebook’s New Look: A Blend of Instagram’s Style

Facebook Compliance: ICE-tracking Page Removed After US Government Intervention

Facebook and Instagram to Reduce Personalized Ads for European Users

InstaDub: Meta’s AI Translation Tool for Instagram Videos

Reclaim Your Account: Facebook and Instagram Launch New Hub for Account Recovery

Meta discontinues Messenger apps for Windows and macOS

Breaking Updates: Meta Connect 2025 Unveils Latest Developments

The Secret strategy of OnePlus

Why DxOMark Smartphone Camera Scores are Wrong

30 Amazing Android SECRETS, TIPS and TRICKS

Android 10 – THIS is why you should be Excited.

The Next OPPO Find X could be very Different…

Honor View20 is a Big Deal – Here’s why

Article 13 – The Future of Mrwhosetheboss.

If THIS is the Huawei P30 Pro…

12 Smartphone Gadgets for 2019.

-

Facebook9 months ago

Facebook9 months agoEU Takes Action Against Instagram and Facebook for Violating Illegal Content Rules

-

Facebook9 months ago

Facebook9 months agoWarning: Facebook Creators Face Monetization Loss for Stealing and Reposting Videos

-

Facebook7 months ago

Facebook7 months agoFacebook’s New Look: A Blend of Instagram’s Style

-

Facebook9 months ago

Facebook9 months agoFacebook Compliance: ICE-tracking Page Removed After US Government Intervention

-

Facebook7 months ago

Facebook7 months agoFacebook and Instagram to Reduce Personalized Ads for European Users

-

Facebook9 months ago

Facebook9 months agoInstaDub: Meta’s AI Translation Tool for Instagram Videos

-

Facebook7 months ago

Facebook7 months agoReclaim Your Account: Facebook and Instagram Launch New Hub for Account Recovery

-

Apple9 months ago

Apple9 months agoMeta discontinues Messenger apps for Windows and macOS