Startups

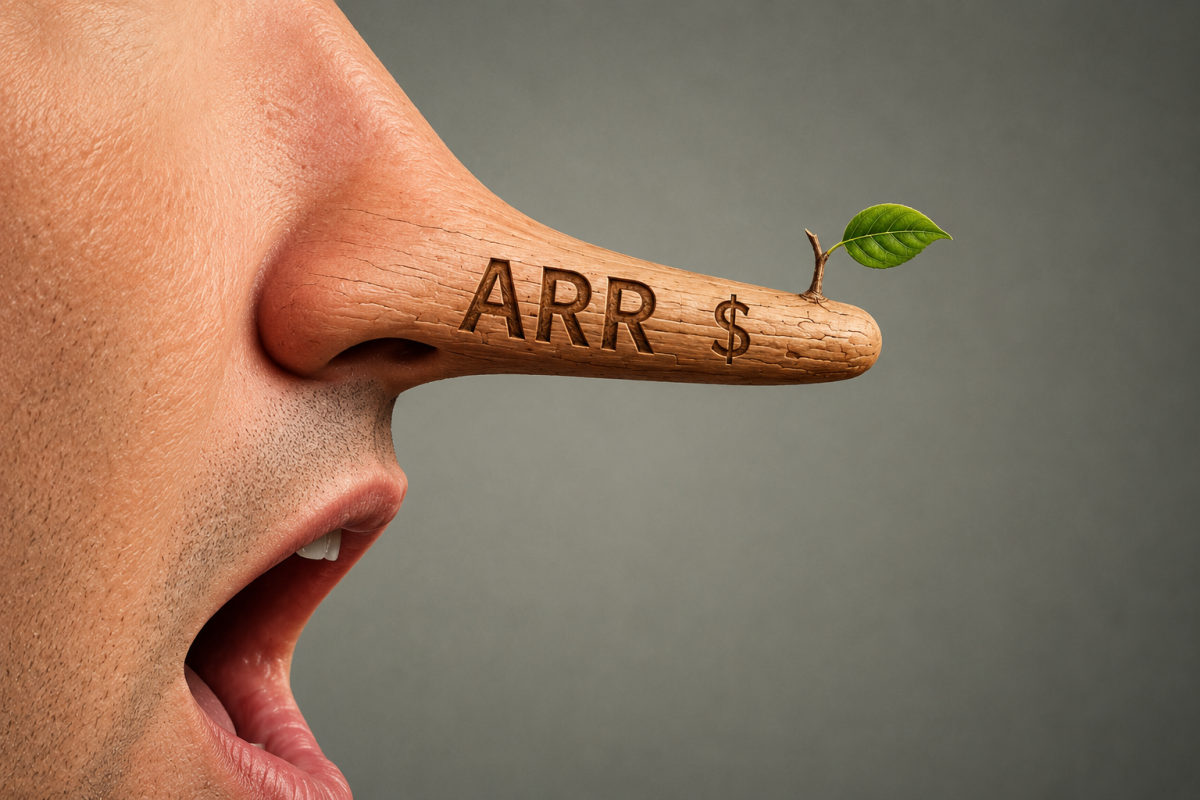

Unveiling the Truth Behind Inflated ‘ARR’ in the AI Startup World

Last month, Scott Stevenson, co-founder and CEO of the legal AI startup Spellbook, took to X in an effort to expose what he called a “huge scam” among AI startups: inflation of the revenue figures that they announce publicly.

“The reason many AI startups are crushing revenue records is because they are using a dishonest metric. The biggest funds in the world are supporting this and misleading journalists for PR coverage,” he wrote in his tweet.

Stevenson isn’t the first to claim that annual recurring revenue (ARR) — a metric historically used to sum up annual revenue of active customers under contract — is being manipulated by some AI companies beyond recognition. Certain aspects of ARR shenanigans have been the subject of multiple other news reports and social media posts.

However, Stevenson’s tweet seemed to have struck a particular nerve within the AI startup community, drawing over 200 reshares and comments from high-profile investors, many founders, and a few headlines.

“Scott at Spellbook did a great job of highlighting some of what you might describe as bad behavior on the part of some companies,” Jack Newton, co-founder and CEO of legal startup Clio, told TechCrunch, adding that the post brought much-needed awareness to the topic, referring to an explanatory post from YC’s Garry Tan about proper revenue metrics.

TechCrunch spoke with over a dozen founders, investors, and startup finance professionals to assess whether the ARR inflation is as pervasive as Stevenson suggests.

Indeed, our sources, many of whom spoke on the condition of anonymity, confirmed that fudged ARR in public declarations is a common occurrence among startups, and how, in many cases, investors are aware of the exaggerations.

Not really revenue, yet

The main obfuscation tactic is substituting “contracted ARR,” sometimes referred to as “committed ARR” (CARR), and simply calling it ARR.

“For sure they are reporting CARR” as ARR, one investor said. “When one startup does it in a category, it is hard not to do it yourself just to keep up.”

ARR is a metric established and trusted since the cloud era to indicate total sales of products where usage, and therefore payments, is metered out over time. Accountants don’t formally audit or sign off on ARR primarily because generally accepted accounting principles (GAAP) focus on historical, already-collected revenue, rather than future revenue.

ARR was intended to show the total value of signed-and-sealed sales, typically multiyear contracts. (Today, this concept tends to go by another name: remaining performance obligations.) Meanwhile, the term “revenue” is typically reserved for money already collected.

CARR is supposed to be another way to track growth. But it’s a much squishier metric than ARR because it counts revenue from signed customers that aren’t onboarded yet.

One VC told TechCrunch that he has seen companies where CARR is 70% higher than ARR, even though a significant chunk of that contracted revenue will never actually materialize.

CARR “builds on the ARR concept by adding committed but not yet live contract values to total ARR,” Bessemer Venture Partners (BVP) wrote in a blog post back in 2021. Critically, though, BVP says, the startup is supposed to adjust CARR to take into account expected customer churn (how many customers leave) and “downsell” (those who decide to buy less).

The main problem with CARR is counting revenue before a startup’s product is implemented. If implementation is lengthy or goes awry, clients might cancel during the trial before all — or any — of the contracted revenue has been collected.

Several investors told TechCrunch that they directly know of at least one high-profile enterprise startup that reported it surpassed $100 million in ARR, when only a fraction of that revenue came from currently paying customers. The rest was from contracts that hadn’t been deployed yet and in some cases may take a long time to implement the technology.

One former employee at a startup that routinely reported CARR as ARR told TechCrunch that the company counted at least one substantial, yearlong free pilot as ARR. The company’s board, including a VC from a large fund, was aware that the revenue from the eventual paying part of the contract had been counted in ARR during the lengthy pilot program, the person said. The board was also aware that the customer could cancel before paying the full contract amount.

The obvious problem with using CARR and calling it ARR is that it is far more susceptible to being “gamed” than traditional ARR. If a startup doesn’t account realistically for churn and downsell, CARR could be inflated. For instance, a startup could offer big discounts for the first two years of a three-year contract and count the whole three years as CARR (or ARR), even though customers may not stick around to pay the higher prices in year three.

The other, more problematic “ARR”

There’s another issue surrounding all those public ARR declarations.

In the world of startups, founders sometimes utilize a different form of measurement known as annualized run-rate revenue, which also goes by the acronym “ARR.” This method involves projecting current revenue over the next 12 months based on a specific period’s earnings, such as a quarter, month, week, or even a day.

However, the use of annualized run-rate ARR can be controversial, especially for AI companies that charge based on usage or outcomes. This approach may lead to misleading calculations as revenue is no longer tied to predictable contracts.

Many experts acknowledge that overstatements in ARR figures are not uncommon, but the rise of AI startups has intensified this practice. With increasing valuations, there is a greater incentive for companies to inflate their ARR numbers.

In today’s AI-driven landscape, startups are under pressure to demonstrate rapid growth like never before. Venture capitalists (VCs) expect exponential expansion rather than traditional incremental growth in annual recurring revenue (ARR).

This emphasis on rapid growth has led some VCs to support startups that present inflated ARR figures to the public. The desire to showcase “runaway winners” and attract media attention can influence investors to turn a blind eye to potential misrepresentations.

While some investors are aware of these discrepancies, they may choose to remain silent to maintain a positive image for their portfolio companies. By endorsing inflated ARR figures, VCs contribute to the perception of their investments as industry leaders, attracting top talent and customers.

Despite the industry’s acceptance of inflated ARR figures, skepticism remains among those familiar with the sector. Some startups find it challenging to believe claims of rapid revenue growth, particularly when reaching significant milestones like $100 million in ARR within a short timeframe.

Certain founders prioritize transparency and accuracy in reporting their revenue figures, opting to disclose actual ARR rather than inflated numbers. By avoiding the use of misleading metrics like contracted ARR (CARR), these startups aim to build trust with investors and stakeholders.

Ultimately, exaggerating revenue figures for short-term gains can have long-term consequences, according to industry experts. Maintaining honesty and integrity in reporting financial metrics is essential for establishing credibility and avoiding potential backlash in the future.

Unleashing the Power: G-POWER’s GP-480 Upgrade Boosts the BMW B58 Engine to 480 HP

Bungie Announces Layoffs Following Conclusion of Destiny 2 Support

Maximize Your Workout with the Sportneer 18Lb Adjustable Weighted Vest: A Comprehensive Review

Strategic Cost-Cutting for MVP Development on a Founder’s Budget: Essential vs. Non-Essential Features

Customise your Android Smartphone – 2019 Edition.

Unleash Your Creativity: Customize Your Samsung Galaxy with This Secret App

Protecting Your Privacy: A Guide to Preventing Meta AI from Accessing Your Instagram Photos

Revolutionary 478kW EV Now Available: Genesis GV60 Prices Revealed

Cloud Bucket Hijacking, Windows LPE Chain, and Global Fraud Bust: A Roundup of 20 Cybersecurity Threats

EU Takes Action Against Instagram and Facebook for Violating Illegal Content Rules

Warning: Facebook Creators Face Monetization Loss for Stealing and Reposting Videos

Facebook’s New Look: A Blend of Instagram’s Style

Facebook Compliance: ICE-tracking Page Removed After US Government Intervention

Facebook and Instagram to Reduce Personalized Ads for European Users

InstaDub: Meta’s AI Translation Tool for Instagram Videos

Reclaim Your Account: Facebook and Instagram Launch New Hub for Account Recovery

Meta discontinues Messenger apps for Windows and macOS

Breaking Updates: Meta Connect 2025 Unveils Latest Developments

Customise your Android Smartphone – 2019 Edition.

Why OnePlus 5 is the Best Cheap 2019 Smartphone.

Can a $100 Smartphone Camera beat $900 Flagships?

Xiaomi Mi 9 UNBOXING!

Samsung Galaxy S10 Plus vs iPhone XS Max

Samsung Galaxy S10 Plus vs Galaxy Note 9

Samsung S10+ vs iPhone XS Max / Mate 20 Pro / OnePlus 6T / Galaxy Note 9 Battery Life DRAIN TEST

Nokia 9 PureView UNBOXING!

Samsung S10’s 3D Sonic Sensor IS GAME CHANGING.

-

Facebook9 months ago

Facebook9 months agoEU Takes Action Against Instagram and Facebook for Violating Illegal Content Rules

-

Facebook9 months ago

Facebook9 months agoWarning: Facebook Creators Face Monetization Loss for Stealing and Reposting Videos

-

Facebook7 months ago

Facebook7 months agoFacebook’s New Look: A Blend of Instagram’s Style

-

Facebook9 months ago

Facebook9 months agoFacebook Compliance: ICE-tracking Page Removed After US Government Intervention

-

Facebook7 months ago

Facebook7 months agoFacebook and Instagram to Reduce Personalized Ads for European Users

-

Facebook9 months ago

Facebook9 months agoInstaDub: Meta’s AI Translation Tool for Instagram Videos

-

Facebook7 months ago

Facebook7 months agoReclaim Your Account: Facebook and Instagram Launch New Hub for Account Recovery

-

Apple9 months ago

Apple9 months agoMeta discontinues Messenger apps for Windows and macOS